In a recent report, “Op waarde geschat? Duurzaamheids-risico’s en -doelen in de Nederlandse financiële sector ” (Estimated at worth? Sustainability risks and targets in the Dutch Financial sector), the Dutch Central bank (DNB) warned that Dutch financial institutions needed to take sustainability risks and targets more seriously. In August 2018, we researched the sustainability reporting of banks and came to a similar conclusion. In this blogpost we will share some of those results and provide quick tips for banks struggling to include aspects of sustainability into data management.

In a review of 25 medium-to-large Dutch financial institutions, the DNB found that only 36% set clearly defined sustainability targets, while only 20% actively monitor progress towards achieving these goals. Those targets include, but are not limited to: conservation of natural life, halting climate-change, future-proof business models (digital) and reducing inequality. Banks’ credits play a crucial role here, because they hold the power to stimulate growth in businesses. If financial institutions report progress on sustainability at all, it is mostly reported using non-standard definitions based on unclear and incomparable characteristics. Furthermore, the DNB states that financial institutions do not have a clear picture of the threats their portfolio faces as a result of a rapidly changing world. Water crises, extreme weather events and cyber-attacks are some examples of risks the financial sector should be preparing for.

Our benchmark study on sustainable finance and data management suggests a similar conclusion. Data management is as an essential first step in order to mitigate risks from ambiguous factors such as climate change. After all, you can only mitigate risks with available data, which necessitates organizing for structural data gathering and realizing sound methodologies upfront. Which is why we developed the Sustainable Finance Data Management (SFDM) Maturity Index. It serves as a tool to investigate how Europe’s biggest banks monitor and report their progress on sustainability targets such as reducing the CO2-output of they companies which they finance.

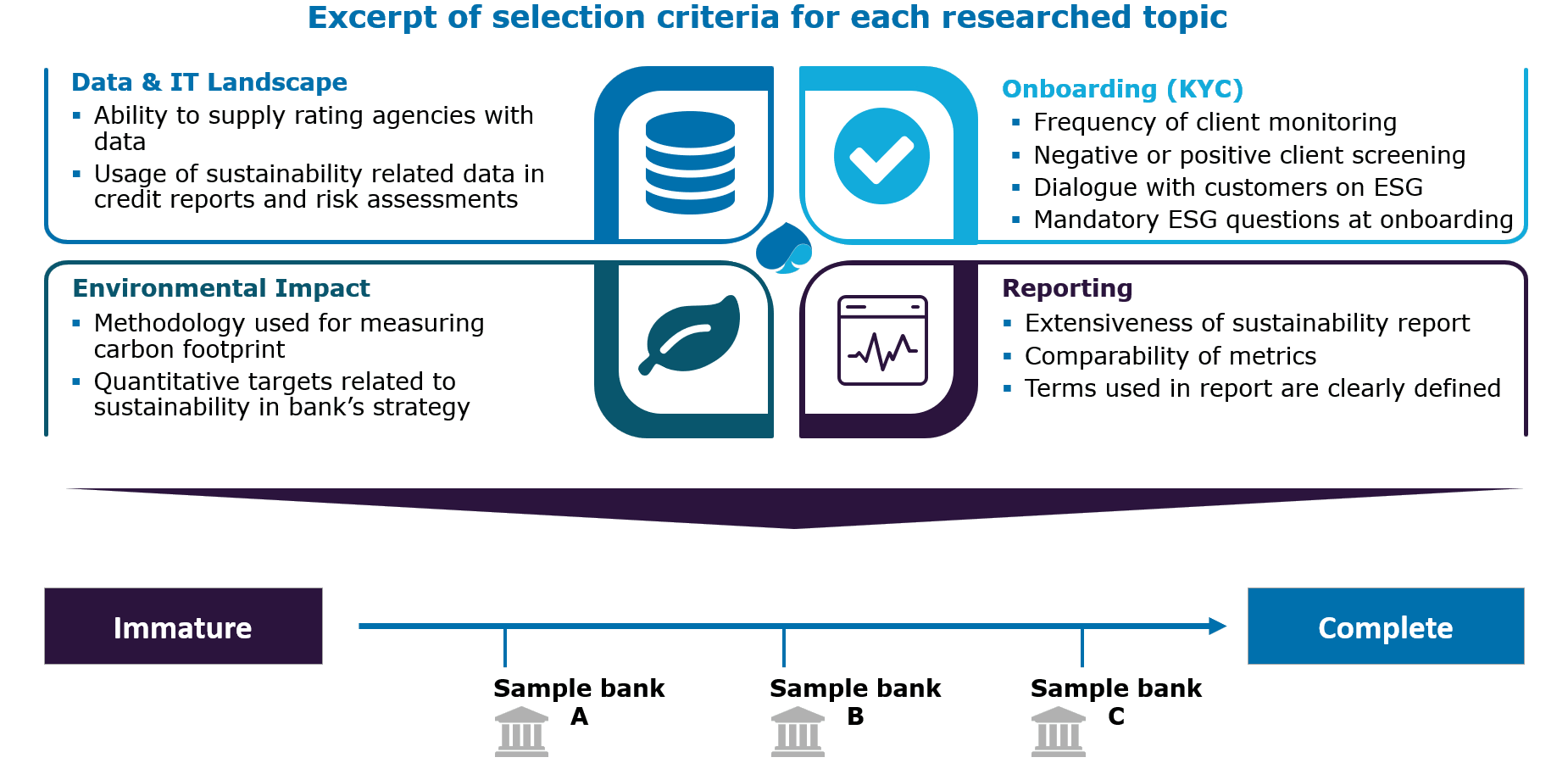

As part of that research, we used the maturity index, to score banks from ‘immature’ to ‘mature’ on four aspects of sustainable data management. We assessed 15 pan-European banks on all four aspects, 40% of banks were immature (low score on 3-4 aspect), another 40% scored somewhat mature. The remaining 20% is divided between mostly Scandinavian and Dutch banks, who were the clear outliers in our research and ranked as mature. For each maturity aspect, we noticed a few recurring trends:

- Data & IT Landscape

Increasing requirements for granularity of data remains an issue for banks. As well as the heterogeneity of multiple data sources. Usually a result of organic growth within the bank, the lack of a strong methodological foundation prevents reconciling sustainability data, and therefore consolidated impact measurement. - Onboarding (KYC)

We agree with DNB that banks need to work towards achieving and monitoring sustainability targets. Currently, KYC has hardly leveraged ways to improve its sustainability. Making use of existing KYC processes to collect the data will accelerate the data availability. - Environmental Impact

There is a lot of talk about the impact of ECG factors both from a perspective of risk and sustainability targets. However, only a few banks define a framework to measure for example environmental risks or carbon footprint reduction. Because of this, it is hard to define a risk appetite or set targets for sustainability. - Reporting

The ‘sustainability’ section of annual reports is long and glamorous, but rarely specific. Some banks are still mostly reporting on direct impact of their own business processes instead of shifting the focus towards the far larger impact of their balance sheets.

In general, sustainability is an important talking point for most banks but seldom transformed into clear tangible objectives.

What can you do to improve your insights into sustainable finance?

From this framework and study, we draw the following conclusions:

- Realize a harmonized model

Stage a uniform methodology for sustainability data to make it comparable and reconcilable. Building on data that’s already available at your bank, will allow for a running start. This way, the quality of both external reports as well as internal reports will be improved. Additionally, monitoring the performance of portfolios on a wider range of indicators becomes easier when data is comparable.

- Work on data completeness for sectors

In line with the global GRI standards, recognize that different (sub)-sectors need different datapoints to measure sustainability impact. For instance, start by covering the data completeness of different subsectors within your Food & Agri portfolio. This way, internal KPI’s may be derived from sector relevant benchmarks.

We recognize the fact that this will not be attained overnight, and especially for the SME and midcrop segment assumptions and sector averages will be needed by lack of specific client input. Strong data governance is required to realize the granularly that exists outside the domain of asset backed financing.

- Data governance to cover diversified SME portfolios

Especially when working with SME clients, banks should expect to provide ample guidance and tooling to coax them towards framework adoption. You need work with them and enrich data through your front-office. This requires processes, partners and strong data governance controls.

In summary, regulators are recognizing the importance of sustainability risks for the financial sector and there is strong evidence that suggests there are only a handful of banks who are well prepared to tackle these head on. However, incorporating sustainability into their business model by better utilizing the data that is available could prove very useful in the long-run.

Are you interested to see how individual banks performed on our maturity assessment? Please don’t hesitate to get in contact with Rob van Dijk.